これってなんで下がったんでしょうか?

返信

投資の参考になりましたか?

パソコン版の掲示板ページをリニューアルし、見た目や機能を一部変更しました。

下記リンクから以前の掲示板もご利用いただけます。

これってなんで下がったんでしょうか?

投資の参考になりましたか?

口から泡でそう

投資の参考になりましたか?

すでに底から二倍

投資の参考になりましたか?

金曜の夜株価見て目を疑ったよね

下の人も言ってるようにUSセルラーとの提携っぽいニュースしかみあたらなくてさっぱりわからなかった

結局すべて売却しました

高配当につられNISAで買ったが、ずるずるもっててかなりのマイナスになってた

前日まで-30%くらいだったのが+20%で売れた、助かったーと思った

これからこの株がさらに暴騰するかもしれんけd、悔いはないわ

高配当でも業績悪いとこに手を出しちゃだめだったよね笑

投資の参考になりましたか?

ティッカーUSMも通信で何やら同じように暴騰してますがわかりませんね🤔

投資の参考になりましたか?

アメリカのボロ株はスグに二倍三倍になるぜw 上場廃止も多い

投資の参考になりましたか?

87%高 www

投資の参考になりましたか?

なんのインサイダーがあるのか

投資の参考になりましたか?

なにがどうしてこうなったか知ってる人いますか?

投資の参考になりましたか?

目が覚めて株価を見たらびっくり‼︎凄い‼︎

投資の参考になりましたか?

本当におめでとう!500万突っ込んだって書いてた時は大丈夫かな?と思ったが正解でしたね〜。

ワイは爆益で今日始末しました〜。

投資の参考になりましたか?

TDS。ベライゾン。AT&T。みんな上がっていく!!!!!!

さげすぎたもんな。。

TDS Telecommunications LLC は、全国の通信ネットワークの評価を実施

約16マイルの鉛被覆ケーブル。

TDS Telecom は、ネットワーク内に存在すると推定される鉛ケーブルの量が非常に限られていることに対処するための次のステップを特定しています。

TDS Telecom は、サービスを提供する地域、州、および連邦の適用されるすべての法律に従うよう努めています。

このプレス リリースには、TDS Telecom の通信ネットワーク内の鉛被覆ケーブルの量に関する推定値が含まれています。

16マイル。約25.7km。

これさ。TDSは鉛ケーブルすくねえよって話じゃないのか???????

ベライゾン。ATT入れて25.7kmしかないわけないよな??????

全部上がってるから。どうせ大した問題じゃなかったってだけかもしれんがな。。

投資の参考になりましたか?

現状の配当利回りだけで判断し参入

吉と出るか凶と出るか

投資の参考になりましたか?

てな訳で1ドル135円切って欲しいなぁ…。

投資の参考になりましたか?

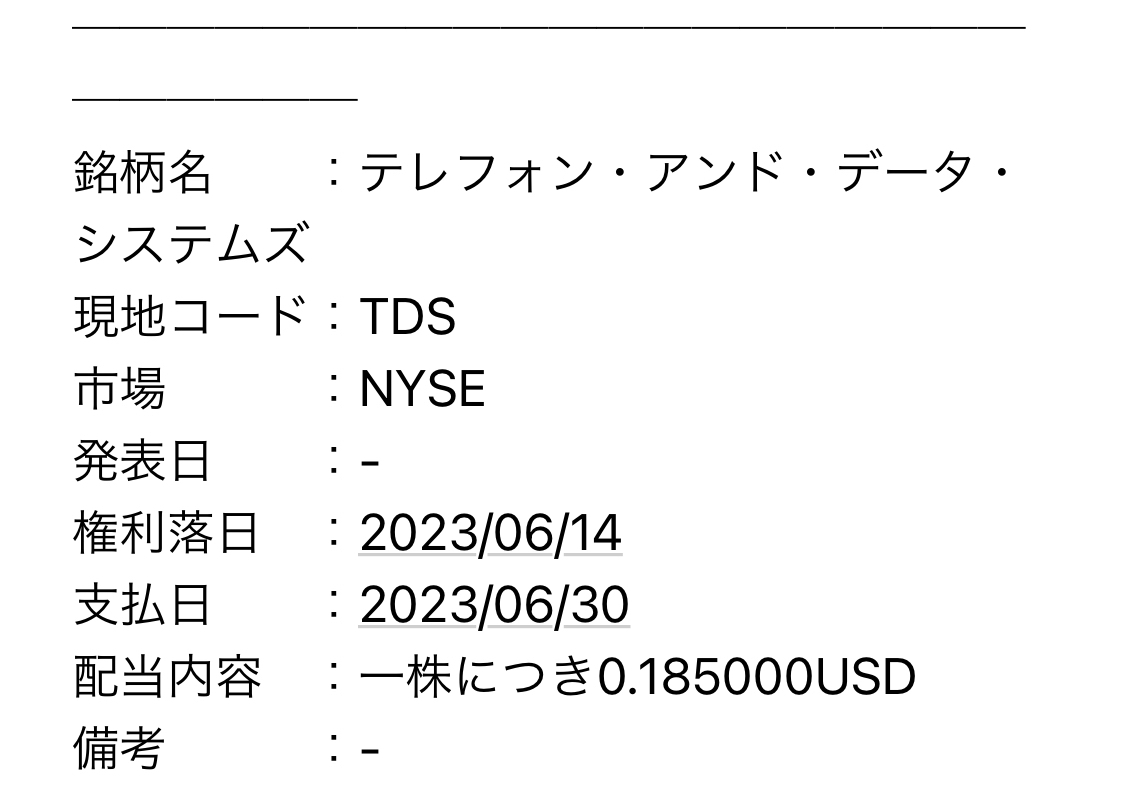

配当金額維持キター!!

強く買いたい

強く買いたい投資の参考になりましたか?

利益が死ぬほど減っている。

米国株を日本株のようにスケベ買いしたらケツの毛まで毟られる。ちょっと今は手を出せない。次の決算まで様子見する

投資の参考になりましたか?

日本株と違って情報得る難度が高過ぎる。

TwitterポチポチしてGoogle翻訳さんで色々翻訳してもイマイチわからん。

Q1決算が悪かったみたいなのは理解したが、基地局が会社より価値が有るから売却しろ!みたいな話も書いてるし、何があったんや…。

配当維持なら買い増ししたいんやがなぁ…。

投資の参考になりましたか?

ワロタw

投資の参考になりましたか?

何が起きたんですか?

投資の参考になりましたか?

何があった??

投資の参考になりましたか?

18ドル75セントで指値入れといて刺されば予定数量買い増し完了😊

投資の参考になりましたか?

今の時期に買うのは良さそう

ただ将来性とかは感じられない

投資の参考になりましたか?

米国株式デビュー者です。

いろいろな銘柄を覗いている中で当銘柄に興味を持ちました。

ここの直近の株価下落が気になっています。

買いたいのですが何があったのか気になって踏ん切りがつかない状況です。

知見のある方よろしければお教えいただけないでしょうか?

投資の参考になりましたか?

過去投稿拝見しました。

私と同じようなスタンスの方がいらっしゃって嬉しいです😊

投資の参考になりましたか?

私も買います!

投資の参考になりましたか?

さて、そろそろ安い値段で買っていくか☺️

投資の参考になりましたか?

テレフォン&データシステムズについて話し合うスレッドです。

スレッドのテーマと無関係のコメント、もしくは他にふさわしいスレッドがあるコメントは削除されることがあります。

textreamのビジネス、株式、金融、投資、または証券に関するスレッドに参加する場合は、Yahoo! JAPAN利用規約を再読してください。

Yahoo! JAPANは情報の内容や正確さについて責任を負うことはできません。

その種の情報に基づいて行われた取引や投資決定に対しては、Yahoo! JAPANは何ら責任を負うものではありません。

投資の参考になりましたか?